The cost of market data, a by-product produced through the compilation and aggregation of pre-and post-trade data by Exchanges, are indisputably rising year-on-year. To understand and raise awareness of these increases, this post will investigate how and why market data costs are rising, the regulatory stance and the consequences of high market data costs.

Why is market data costs rising?

Stock exchanges have evolved tremendously over the last few decades, especially during the 1990s when digital and virtual advancements meant data could be exchanged instantly between different organizations. It was these advancements that granted stock exchanges the monopolistic ability (IOSCO 2020:9) to monetize and control access to market data as an additional source of revenue.

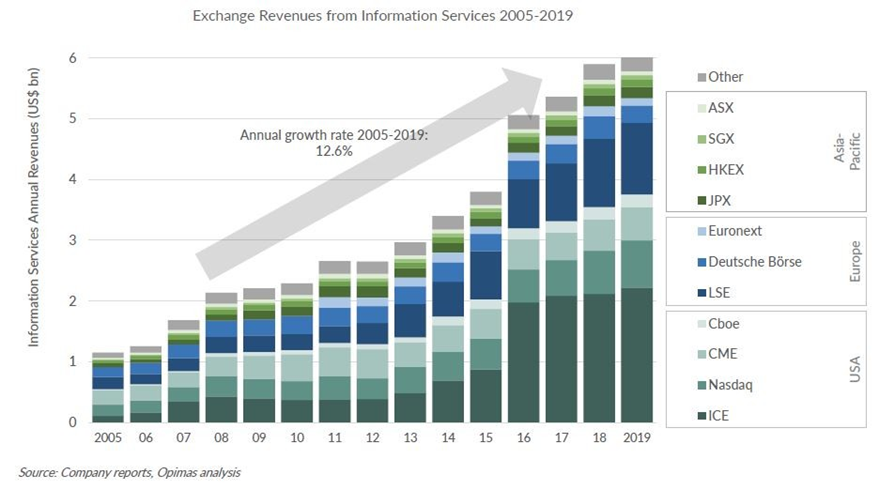

The revenue generated by market data, managed by Information Services, has grown massively over the last 15 years. According to a recent report, Information Services generated just over US$1 billion in 2005 and by 2019 the figure had skyrocketed to just over US$6 billion. An annual growth rate of roughly 12.6%, which contrasts the diminishing revenue of data consumers over the past decade.

The revenue generated by market data, managed by Information Services, has grown massively over the last 15 years. According to a recent report, Information Services generated just over US$1 billion in 2005 and by 2019 the figure had skyrocketed to just over US$6 billion. An annual growth rate of roughly 12.6%, which contrasts the diminishing revenue of data consumers over the past decade.

Given the rising revenue levels and minimal cost to produce market data at Exchanges, the report estimates an impressive operating margin of 76% and eye-watering profit margins that more than double major data vendors or treble that of major investment banks.

How are market data costs rising?

The cost of market data is predominantly decided by Exchanges through various access fees. Any changes to the fees require 3-months written notice in advance from the supplier and usually involves either an additional type of fee or an increment to existing fees.

A notice served by the CME Group, on 30th September, is a prime example that demonstrates how the cost of market data is increasing. Aside from ‘adjusting’ 4 existing fees, the notice arbitrarily introduces 2 additional fees – one of which relates to distributing historical data, a service that has always remained free among major exchanges, including the ICE USA, Eurex, Euronext, and Nasdaq OMX Nordic exchanges:

| Adjusted fees: | Additional fees: |

|---|---|

|

|

Exchange Data International (EDI), has written to the CFTC, the heads of the relevant Committees of the US House of Representatives, and the US Senate – which oversee the CFTC – requesting an investigation into the CME Group’s (CME) plans to charge for what has always been a no-fee service.

Get involved and see how you can help fight the rising cost of market data. Contact Jonathan Bloch, CEO at EDI, on Info@exchange-data.com.

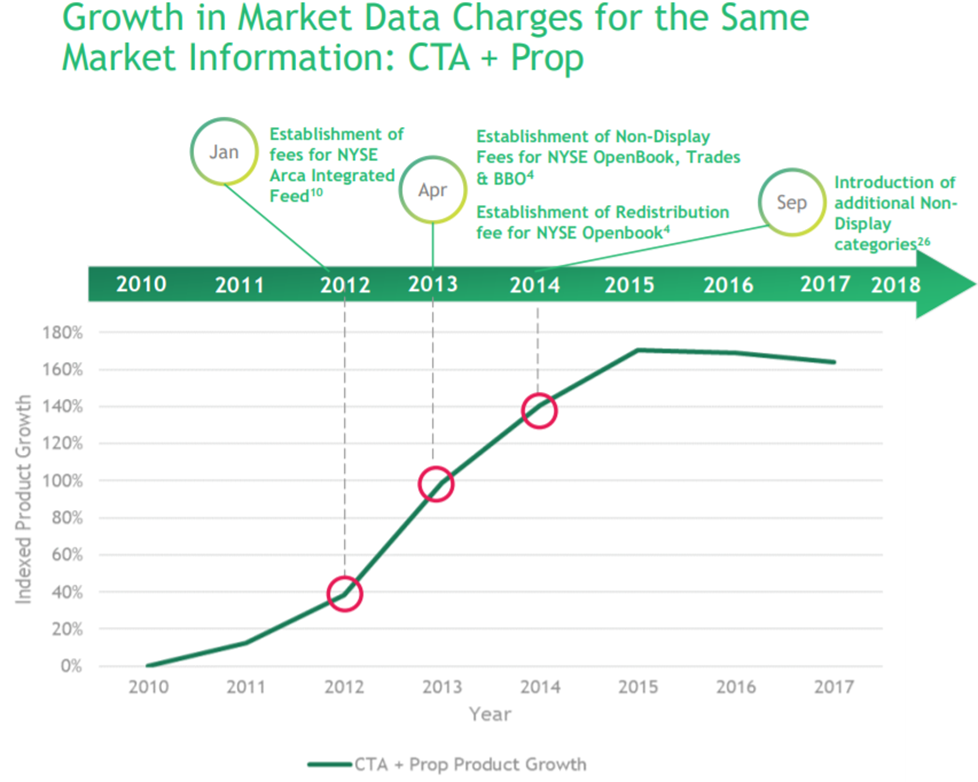

To further demonstrate the increasing number of fees, a recent study on the NYSE by SIFMA (2018:18) found the average number of charges firms incurred increased from roughly 80 line items in 2010 to over 200 in 2017 for the same market information. The study proceeded to investigate NYSE proprietary data fees between 2010-2018 and discovered the total cost to access market data had shot up during this period by 612% to 4,119%, depending on the business model and variable datasets, as a combined result of fee increases and additional charges.

What are the consequences of high data costs?

There are several undesirable consequences of high market data costs, the most obvious and direct would be the consumer’s only available course of action – limiting data charges by restricting the use of market data (Copenhagen Economics 2018:28) or scaling back data purchases to a minimum – sometimes at economically suboptimal levels (Market Data Costs 2020:3). Both subsequently has a knock-on effect that reduces transparency, competition and lower market integration, which accumulates into wider repercussions such as:

- Less informed markets

- Less liquidity

- Higher volatility

- Weaker competition

- Higher costs of capital, especially among smaller firms

The regulatory stance

Supervisory authorities in the United States and Europe have yet to introduce regulatory policies on the issue but have increasingly taken note of the situation. This was demonstrated in a 2018 public statement where SEC repealed an Exchanges’ additional fees on the grounds of insufficient “factual and legal support” (Clayton 2018). However, despite supervisory intervention, nothing beyond guidance has been published and the issue remains largely unresolved.

Supervisory authorities in the United States and Europe have yet to introduce regulatory policies on the issue but have increasingly taken note of the situation. This was demonstrated in a 2018 public statement where SEC repealed an Exchanges’ additional fees on the grounds of insufficient “factual and legal support” (Clayton 2018). However, despite supervisory intervention, nothing beyond guidance has been published and the issue remains largely unresolved.

In 2019, the U.S. Securities and Exchange (SEC) issued guidance on changes to fees for market data where it states fees be reasonable, equitably allocated, not unfairly discriminatory and not an undue burden on competition.

In March, the UK Financial Conduct Authority (FCA) issued a Call for Input that sought to find whether users have concerns with the way trading data, benchmarks and vendor services are priced and sold. The FCA also wanted to understand how innovations in data were generated and used, the value offered to market participants and whether data were sold and priced competitively.

In November, the European Securities and Markets Authority (ESMA) launched a consultation paper that sought input from market participants for guidance on the requirement to publish market data on a reasonable commercial basis and to make market data available free of charge 15 minutes after publication.

What solutions have been proposed?

In the absence of a regulatory solution, participants have proposed solutions that target capping revenue, not price, by aligning the costs of producing market data with the cost of market data fees. This is well illustrated by Copenhagen Economics’ (2019:2) so-called Long Run Incremental Cost model (LRIC+).

Romy Threadgold is the Head of Marketing at Exchange Data International (EDI), where she has been shaping the company’s marketing strategy for over six years. With extensive experience in the financial data industry, Romy is a key driver of EDI’s brand development, client engagement, and communications initiatives.

As a seasoned marketing professional, Romy’s strategic insights and innovative approach continue to solidify EDI’s reputation as a leading provider of financial data